The research of University of Kent Economist, Dr Christian Siegel and Zsófia L. Bárány of the Central European University, Viena have been cited in the … Read more

The research of University of Kent Economist, Dr Christian Siegel and Zsófia L. Bárány of the Central European University, Viena have been cited in the … Read more

Dr Alfred Duncan and Professor Charles Nolan discuss Adam Smith’s vision for banking and try to deduce how Smith might have approached some current issues … Read more

We are hosting the third edition of our workshop, this time a collaboration with joint with the Banks of England and Bristol University and invite … Read more

As the Chancellor finds himself under pressure because of his £43bn tax-cutting programme, it is understood that the Treasury is weighing up a number of … Read more

How should we interpret the U-turn on the abolition of the 45p rate for high income earners? ‘This is more a political move than one … Read more

The annual Money Macro and Finance conference, was hosted here at Kent with top current and former policymakers and academics speaking about the current global … Read more

The Macroeconomics, Growth and History Centre (MaGHiC) are excited to welcome more than a hundred delegates on campus for the 53rd Annual MMF Conference on … Read more

Professor Miguel León-Ledesma has collaborated with Laura Puzzello and Adina Ardelean, in this VoxEU column on the complex interaction between sectoral shocks, sectoral specialisation, and geographic diversification … Read more

Recent Guy Tchuente research shows the importance of local knowledge in the provision of publicly financed goods. Dr Guy Tchuente‘s research is included in a … Read more

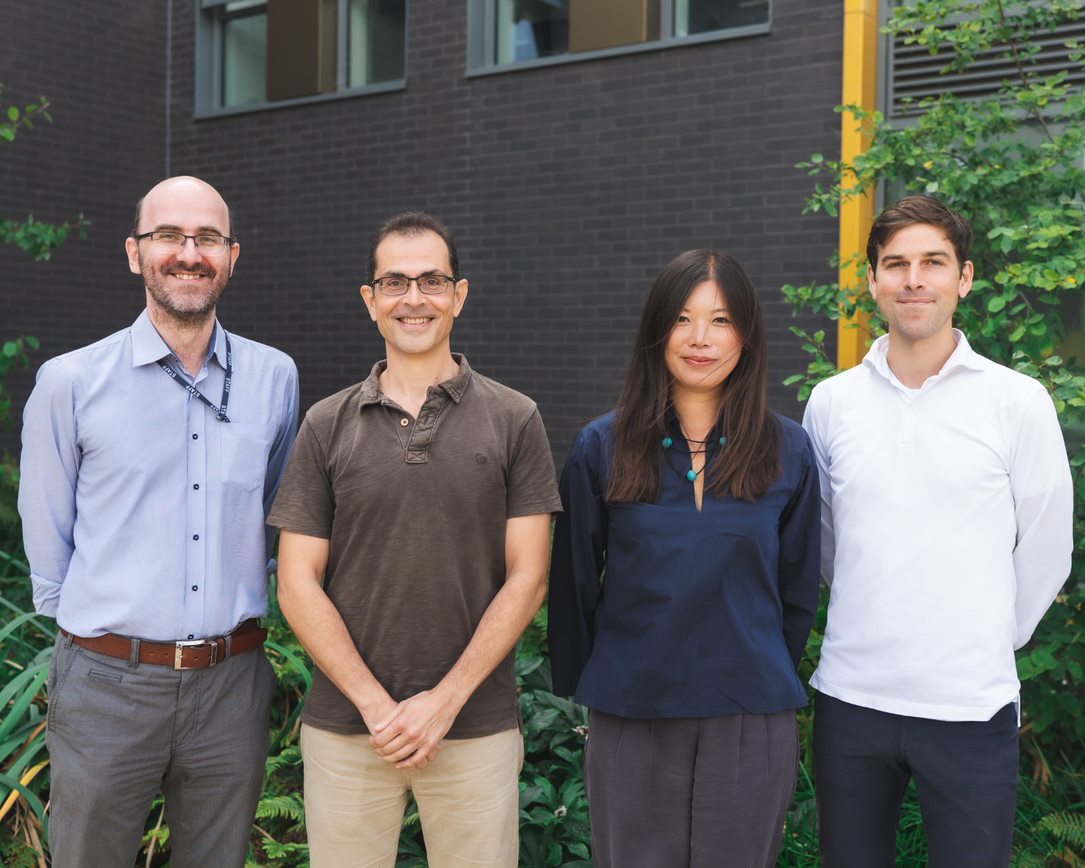

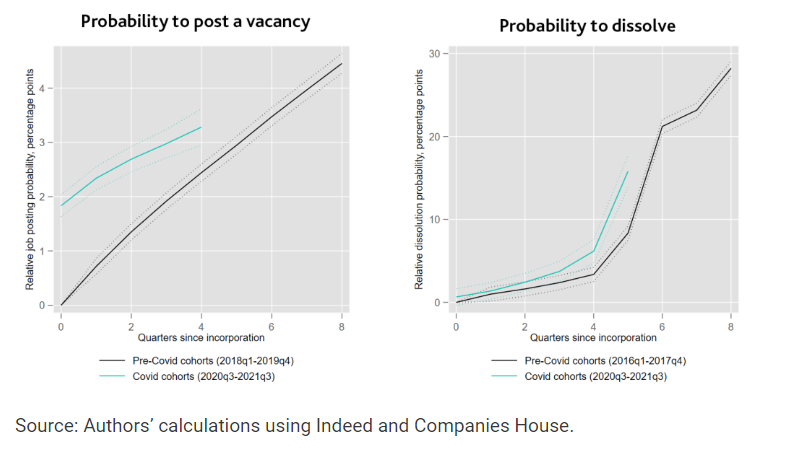

Dr Anthony Savagar has collaborated with Saleem Bahaj from the Bank of England’s Research Hub and Sophie Piton who works in the Bank of England’s … Read more