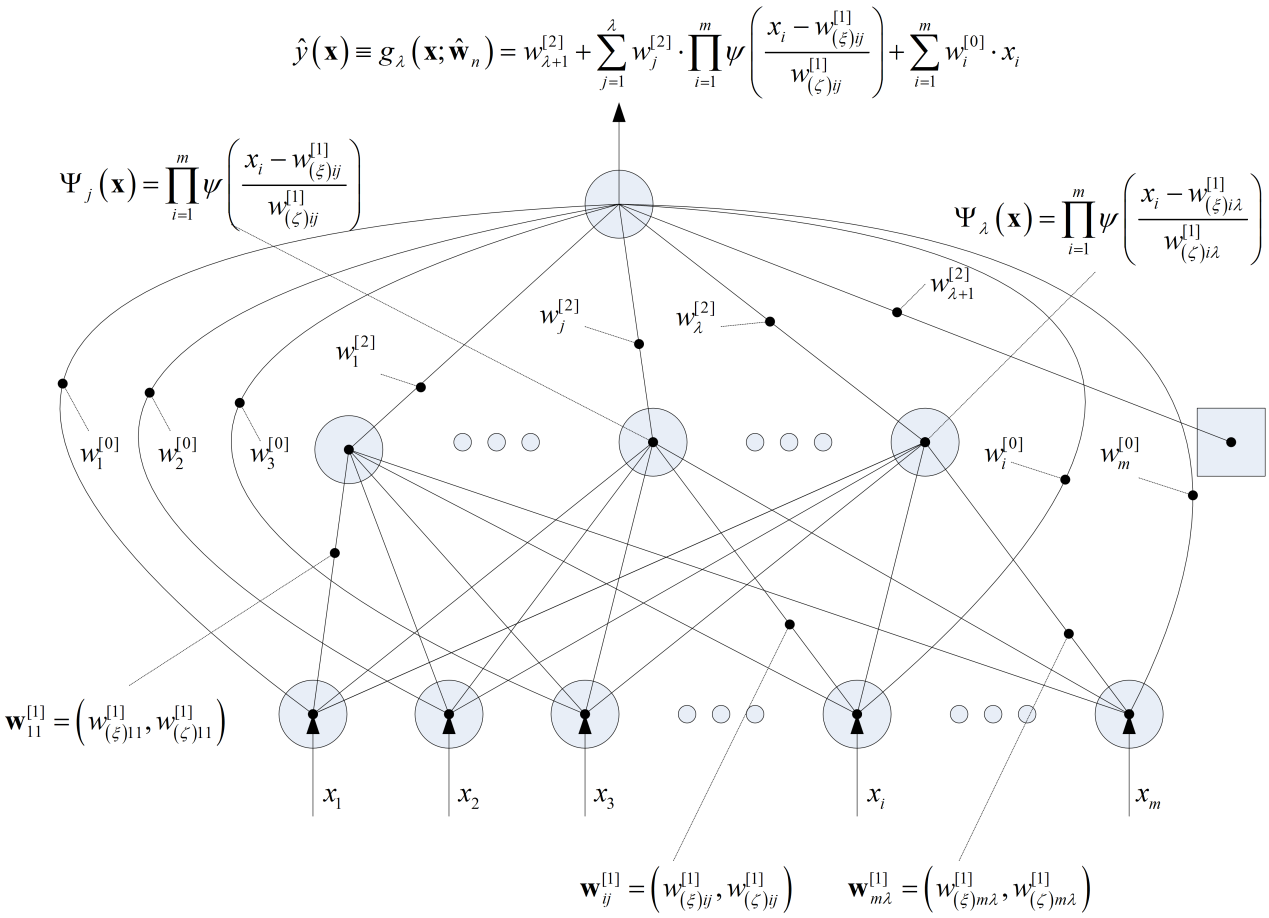

A Wavelet Network

The purpose of this study is to develop a model that describes the dynamics of the daily average temperature accurately in the context of weather derivatives pricing. More precisely, we compare two state-of-the-art machine learning algorithms, namely wavelet networks and genetic programming, with the classic linear approaches that are used widely in the pricing of temperature derivatives in the financial weather market, as well as with various machine learning benchmark models such as neural networks, radial basis functions and support vector regression. Continue reading